Illinois House proposes amendment for medical cannabis taxes

We recently reported on the new adopted cannabis tax amendments stated in the Illinois Register and Flinn Report. Today, Representative Sonya M. Harper introduced the first cannabis amendment of the new legislative session. House Bill 4465 provisions concern rate of taxes for registered medical cannabis patients.

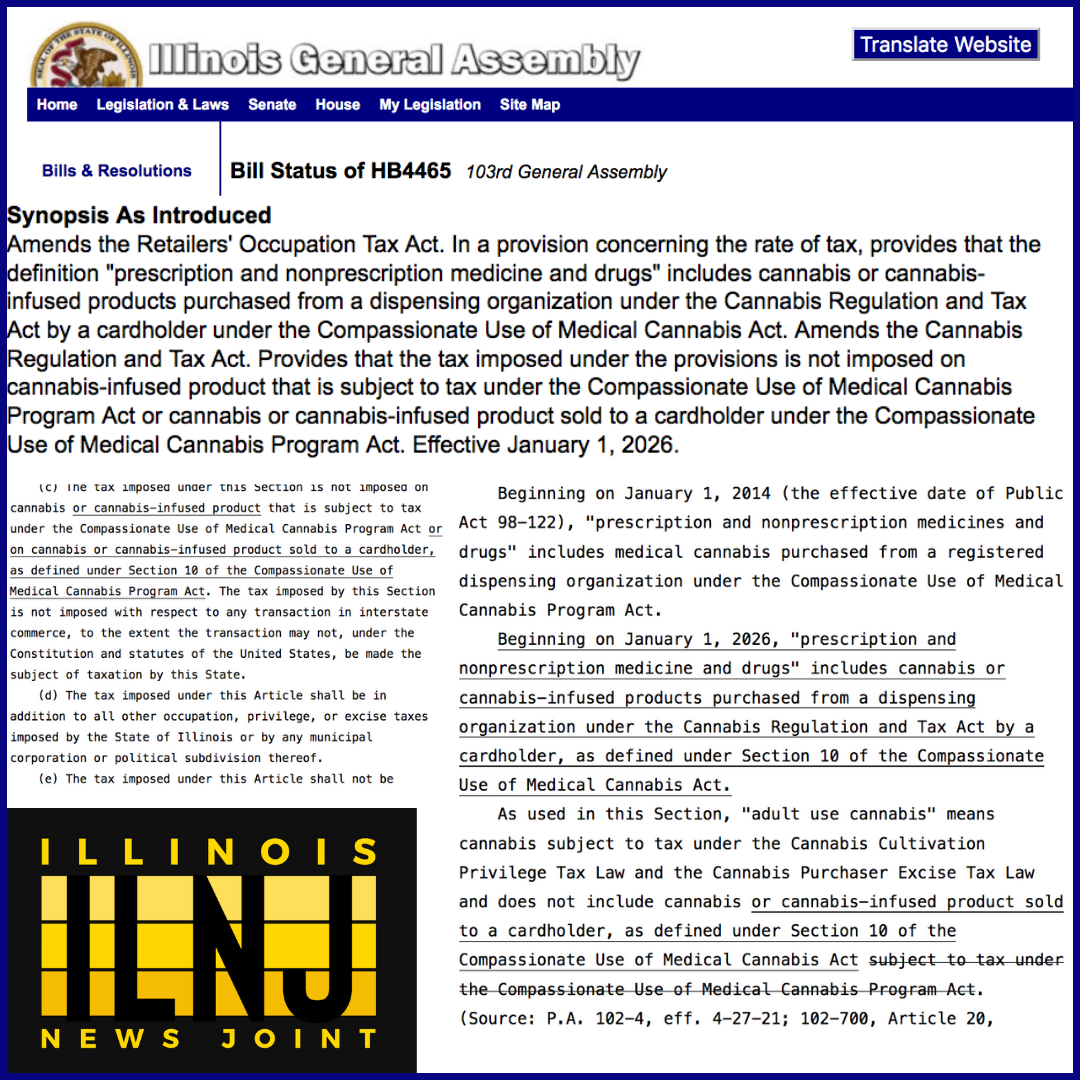

The first additional wording in HB4465 includes, “Beginning on January 1, 2026, ‘prescription and nonprescription medicine and drugs’ includes cannabis or cannabis-infused products purchased from a dispensing organization under the Cannabis Regulation and Tax Act by a cardholder, as defined under Section 10 of the Compassionate Use of Medical Cannabis Act.”

After the wording, “As used in this Section, ‘adult use cannabis’ means cannabis subject to tax under the Cannabis Cultivation Privilege Tax Law and the Cannabis Purchaser Excise Tax Law and does not include cannabis,” the new provision deletes the words, “subject to tax under the Compassionate Use of Medical Cannabis Program Act” and replaces them with, “or cannabis-infused product sold to a cardholder, as defined under Section 10 of the Compassionate Use of Medical Cannabis Act.”

Amends the Retailers’ Occupation Tax Act. In a provision concerning the rate of tax, provides that the definition “prescription and nonprescription medicine and drugs” includes cannabis or cannabis-infused products purchased from a dispensing organization under the Cannabis Regulation and Tax Act by a cardholder under the Compassionate Use of Medical Cannabis Act.

The last wording involves taxation for cannabis-infused product and provides that tax imposed under the provisions is not imposed on cannabis-infused product that is subject to tax under the Compassionate Use of Medical Cannabis Program Act or cannabis or cannabis-infused product sold to a cardholder under the Compassionate Use of Medical Cannabis Program Act. The underlined words (below) have been added to this provision. “The tax imposed under this Section is not imposed on cannabis or cannabis-infused product that is subject to tax under the Compassionate Use of Medical Cannabis Program Act or on cannabis or cannabis-infused product sold to a cardholder, as defined under Section 10 of the Compassionate Use of Medical Cannabis Program Act. The tax imposed by this Section is not imposed with respect to any transaction in interstate commerce, to the extent the transaction may not, under the Constitution and statutes of the United States, be made the subject of taxation by this State.”

The 103rd General Assembly started today and scheduled for adjournment May 24.

For more Illinois cannabis industry news, visit here.

To find cannabis-friendly events in Illinois, visit here.

For Illinois News Joint reviews, visit here.